Plan around variable pay without waiting for every month to look the same.

At a glance

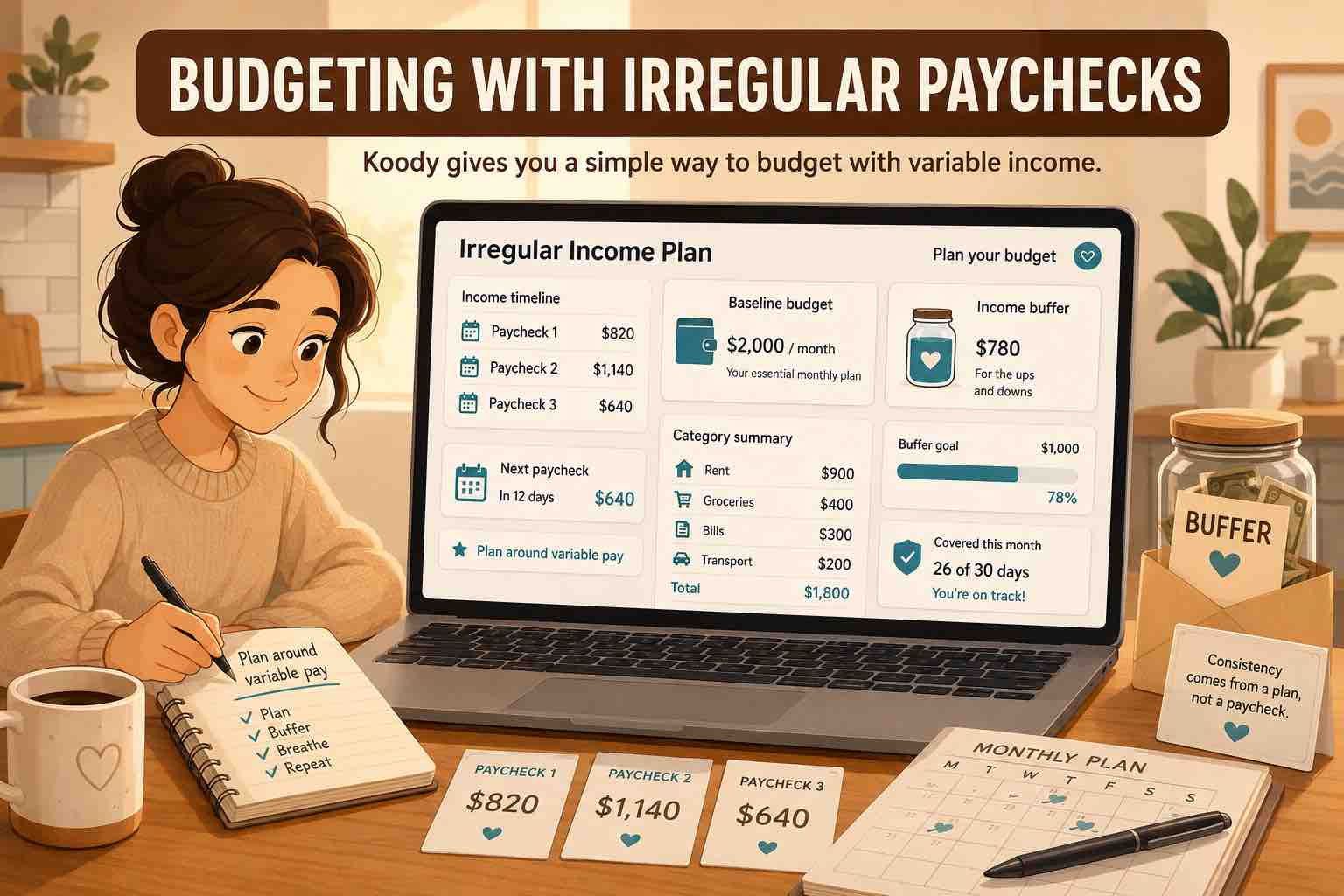

Irregular income budgeting works when you stop pretending every month will look the same. Build from a conservative baseline, use stronger paychecks to create a buffer, track recurring bills before they hit, and review your plan when money lands.

Koody helps you do that with budgets, categories, recurring bills, upcoming transactions, transaction imports, manual entry, weekly reviews, and Koody AI.

If your income changes from week to week, a traditional monthly budget can feel like a guess. Freelancers, gig workers, commission-based roles, seasonal workers, and people with multiple income streams all face the same problem: the bills are fixed, but the paychecks are not.

Budgeting with irregular paychecks is a cash flow problem, not a motivation problem. The solution is to set a baseline income and build a buffer fund so your plan starts with money you can actually count on, even in a slower month.

This guide shows a simple irregular income budgeting system that protects essentials first, then helps you make smart choices with the rest.

Step 1: Find your baseline income

Start by finding your baseline income, the floor you can count on even in a slower month. Some people call this an income floor or minimum viable income. Look at recent income deposits, invoices, or payment summaries to see what actually hits your accounts.

A simple approach is to review the last 6 to 12 months, note each month's total, and choose a conservative number such as your lowest month or a lower-than-average month. That becomes the number you build your variable income budget around.

Keep this number separate from your best months. The baseline is not a goal or a prediction. It is the amount your budget should survive on before bonuses, extra shifts, late invoices, or stronger client months arrive.

Step 2: List your minimum monthly burn

Next, list the expenses that must be paid every month. This is your minimum monthly burn, also called fixed expenses. It includes essentials like housing, utilities, insurance, food, transportation, and debt payments.

Rent or mortgage

Utilities, phone, and internet

Insurance and minimum debt payments

Groceries and essential transport

Childcare or critical subscriptions

The goal is to make sure your baseline income covers this minimum burn. If it does not, you can adjust the baseline, reduce a few essentials, or build your buffer until it does.

In Koody, you can mark subscriptions and bills as recurring so they show up ahead of time in your Upcoming Transactions.

Upcoming transactions help you see bills, subscriptions, and expected income before you spend the next paycheck.

Step 3: Build an income buffer

A buffer turns irregular paychecks into steady cash flow. When you earn more than your baseline in a strong month, do not expand your lifestyle immediately. First, move the extra into a buffer category or separate account.

A separate savings account can make the buffer visible while your checking account covers current spending.

Over time, that buffer smooths your low months. You can even pay yourself a steady salary from it, which makes your budget feel like a regular paycheck again.

This is often called income smoothing, and it is the single biggest stress reducer for variable income.

If you want extra structure, route all income into a holding account, then transfer your baseline amount into your spending account on a set schedule. It turns irregular paychecks into a steady monthly plan.

Step 4: Fund true expenses with sinking funds

Irregular bills are not surprises. They are just future expenses you can plan for. Sinking funds, sometimes called true expenses, make this easy by spreading big costs across the year.

Annual fees, memberships, or tax payments

Car repairs, maintenance, and insurance renewals

Gifts, holidays, and travel

Medical or home expenses

Break each cost into a monthly amount, then set that aside every month. In Koody, you can create categories for each sinking fund and track progress alongside your regular budget.

Category views make sinking funds visible beside the rest of your budget.

Step 5: Make a paycheck plan

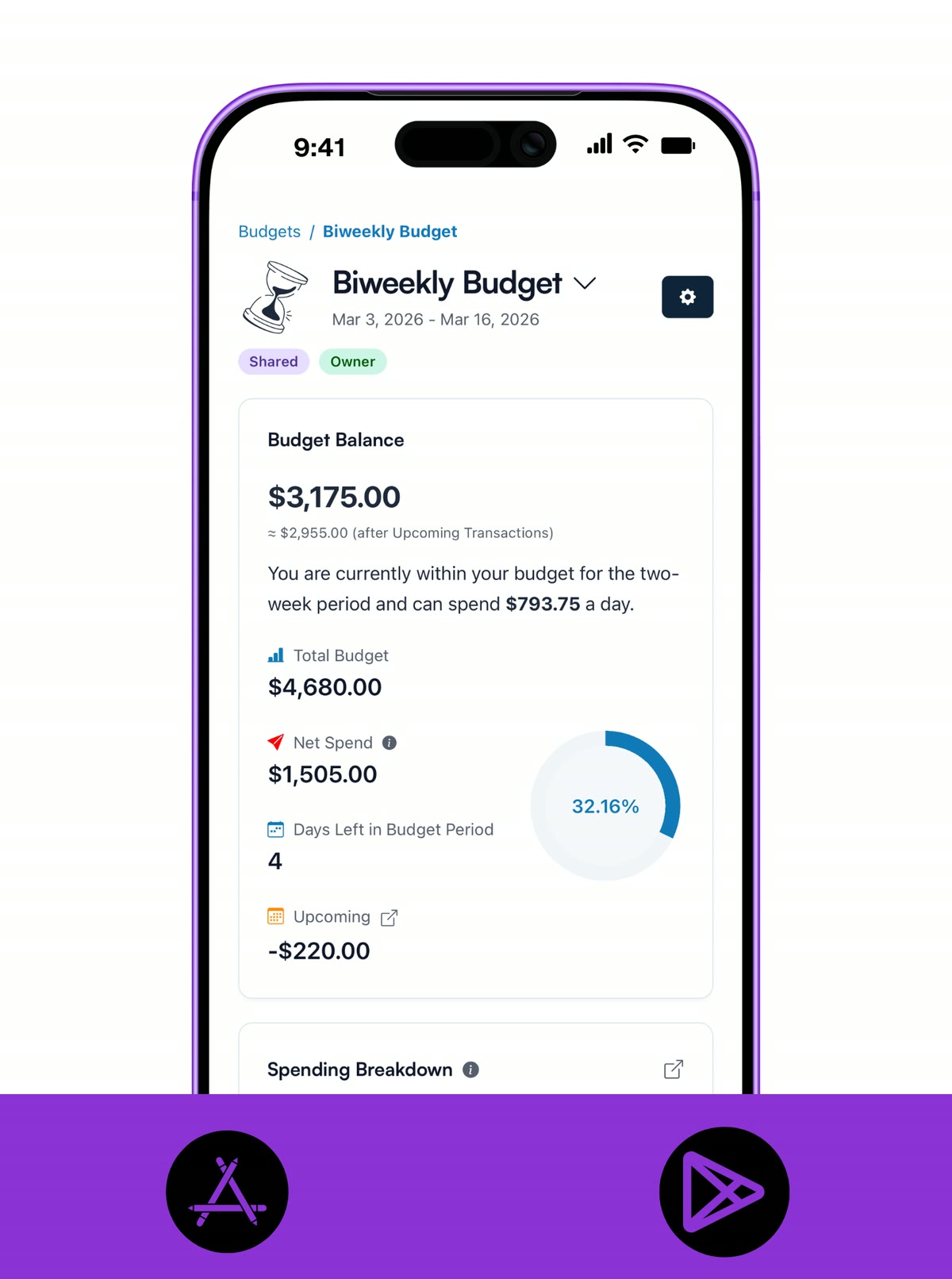

Every time a paycheck arrives, assign it on purpose. Start with essentials, then buffer, then sinking funds, and finally flexible spending. This is a simple version of budgeting by paycheck that works well for irregular income.

A biweekly budget gives each paycheck a job before the next one arrives.

A quick rule of thumb: plan with a low income estimate, then decide how to use extra income when it arrives. If a category matters later, fund it before you fill optional categories now. That keeps slow months from turning into emergencies.

Essentials and minimum payments first.

Taxes and business costs if you are self-employed.

Buffer fund top-ups.

Sinking funds for true expenses.

Flexible spending and extras.

You can use Koody budgets and categories to track each paycheck plan, or keep it lightweight and just track your spending against the baseline in your spending tracker.

Step 6: Review weekly and adjust

Irregular income budgets work best with short check-ins. A weekly review helps you spot overspending early and reassign money before it becomes a problem.

Look at your categories, upcoming bills, and buffer balance. If income slows, pause flexible spending. If a strong paycheck lands, refill sinking funds or add to savings. This simple cash flow forecasting habit keeps your variable income budget steady.

You can also ask Koody AI questions like "What did I spend on essentials last month?" or "How much buffer do I have?" to keep your plan grounded in real data.

Koody AI can help you review spending, category pressure, and next steps when income changes.

Budget around the income you actually receive.

Koody helps you plan with categories, recurring bills, transaction imports, manual entry, weekly reviews, and Koody AI, so your budget can adjust when variable pay arrives.

1. What is the best budgeting method for irregular income?

The best method is a bills-first plan built around a conservative baseline income. Cover essentials first, build a buffer with stronger paychecks, then assign the rest of each paycheck on purpose.

2. Should I budget based on my lowest month or my average income?

Start with a conservative baseline, such as your lowest recent month or a lower-than-average number. When a higher paycheck arrives, you can add the extra to savings, sinking funds, debt, or flexible categories.

3. How do I build a buffer for irregular paychecks?

Use higher-income months to save an extra cushion in a separate buffer category or account. The goal is to make slower months less stressful because your bills are already covered.

4. How do I handle bills that do not happen every month?

Use sinking funds. Divide annual, quarterly, or seasonal bills into monthly amounts, then set that money aside before the bill arrives.

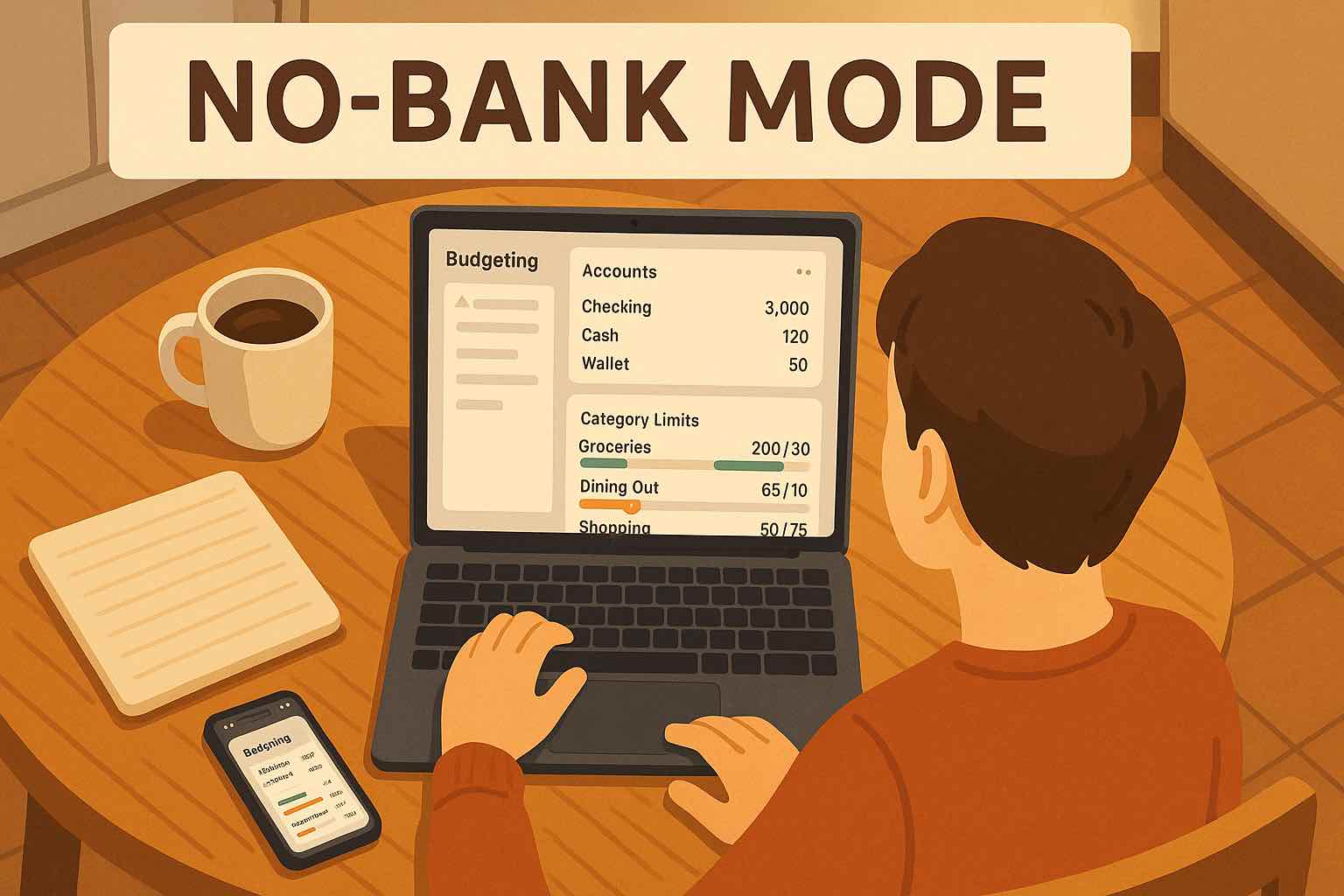

5. Can I budget with irregular income without linking my bank?

Yes. Koody lets you use transaction imports and manual entry without linking your bank, so you can still build a solid irregular-income budget.

6. How should freelancers budget for taxes with irregular income?

If taxes are not withheld, set aside a separate tax category each time you get paid. As you learn your actual tax rate, adjust the percentage before you spend the money elsewhere.

7. What if I have multiple income streams?

Track each stream separately, then combine them to find a conservative baseline. This keeps your plan stable when one client, job, platform, or income source slows down.

8. Can I use Koody for variable income?

Yes. Koody works as a flexible budgeting app for irregular income, with categories, recurring bills, upcoming transactions, imports, manual entries, and weekly reviews you can adjust when variable pay arrives.

9. Does a budget by paycheck app help with irregular income?

Yes, if it helps you decide what each paycheck needs to cover before you spend it. That is useful when income arrives unevenly but bills stay predictable.

Budget with irregular income in Koody.

Budget with irregular income in Koody. Set a baseline income, build a buffer, track recurring bills, plan each paycheck, and adjust when money lands.