There are two simple ways to create a budget in Koody: ask Koody AI to do it for you, or create the budget yourself from the Budgets tab.

If you want the fastest path, ask Koody AI. You can describe what you want in plain English, review the budget in the chat, ask for changes, and save it when it looks right. If you prefer to set every date, account, category, and limit by hand, you can still do that yourself.

Both routes lead to the same kind of Koody budget: a date range, selected accounts, categories, and spending limits that help you compare your real spending against the plan you made.

Option 1: Ask Koody AI To Create It

Koody AI is the easiest place to start if you do not want to fill out a form. You can ask for a budget the same way you would ask a person for help:

- Create a monthly budget for me.

- Create a weekly budget for me.

- Create a 50/30/20 budget.

- Create a budget from my spending history.

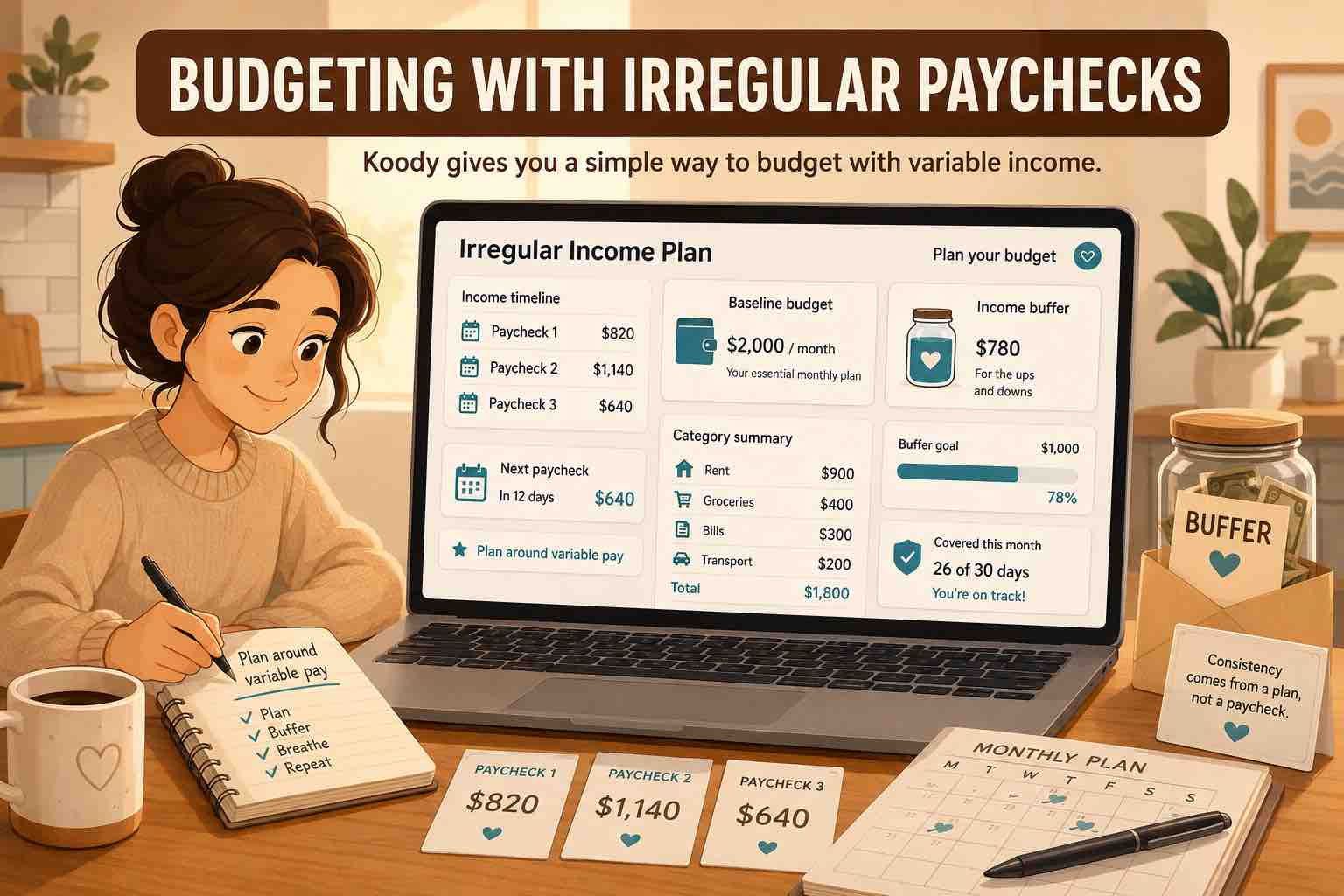

- Align my budget with my payday.

- Make my current budget stricter.

If you already have transactions in Koody, Koody AI can use your spending history as a starting point. It can look at your categories, recent spending, existing budgets, and account scope, then build a practical budget for you to review.

If you do not have much spending history yet, Koody AI can still help. It may ask you to import transactions, or it may ask a few simple questions about your rent, groceries, bills, subscriptions, savings goals, and regular spending. That way, the first budget is based on something real instead of a random template.

The useful part is that you can keep talking. If groceries look too high, ask Koody AI to lower them. If the whole budget feels too tight, ask for a more relaxed version. If you want a weekly budget, a payday-aligned budget, or a stricter rest-of-month plan, say that. Koody AI can explain what changed and keep refining the budget with you.

Option 2: Create It Yourself

If you already know the exact plan you want, you can create the budget yourself. Open the Budgets tab and choose New. Koody will ask for the same core pieces: budget name, dates, accounts, categories, and limits.

1. Name The Budget

Give the budget a name you will recognize later. Simple names work well, such as "Monthly Budget", "June Household Budget", "Vacation Budget", or "Groceries And Eating Out".

2. Pick The Dates

Choose the start and end dates for the budget. A monthly budget might run from the first day of the month to the last day. A payday budget might run from one paycheck to the next. A trip or event budget might only cover a few days.

If you want the budget to repeat, use the recurring option instead of treating it as a one-off budget with a fixed end date.

3. Choose The Accounts

Pick the accounts this budget should watch. You might include your main checking account, a credit card, or the household accounts that carry shared expenses. Koody only counts matching transactions from the selected accounts and date range.

4. Choose Categories And Limits

Select the categories you want to include, then set a spending limit for each one. You can keep this simple with a few everyday categories, or make it more detailed if you want closer control.

As you add limits, Koody shows the total budget. This helps you see whether the full plan makes sense before you save it.

5. Add Notes And Save

Notes are optional, but they can be useful when you look back later. You might write why a category is higher than usual, what you are trying to cut back on, or what changed that month.

When everything looks right, save the budget. Koody will start tracking matching transactions against the limits you set.

Customize Dates, Accounts, Categories, And Limits

A good budget should fit how you actually live. In Koody, you can shape the budget around the period, accounts, and categories that matter for that plan.

Dates decide which transactions count. Accounts decide which money activity the budget can see. Categories decide what the budget is measuring. Limits decide what "on track" means for each category.

Koody AI can help with those choices, too. You can ask it to align a budget to payday, make a weekly version, reduce a few category limits, make the whole budget stricter, loosen it slightly, or explain which categories look unrealistic based on your spending.

You can also ask Koody AI to help edit a current budget. For example, you might ask it to change dates, adjust category limits, or make the plan stricter for the rest of the month.

Use Your Budget And Keep Improving It

After the budget is saved, Koody tracks spending against the categories, dates, and accounts you chose. You can see which categories are still comfortable, which ones are close to the limit, and which ones need attention.

You do not have to get the first version perfect. Budgets are easiest to use when they start with realistic numbers and improve as you learn. If a category is clearly wrong, change it while the budget is active. If your next budget needs a different structure, ask Koody AI to help adjust it before you save the next one.

When a budget expires, it becomes a record of that period. You can still open it, review the original limits, see the actual spending, and use what you learned to make the next budget better.

FAQs: Budgets In Koody

1. What is the easiest way to create a budget in Koody?

The easiest way is to ask Koody AI to create one for you. You can say something simple like "Create a monthly budget for me" or be more specific, such as "Create a weekly grocery budget" or "Create a 50/30/20 budget." Koody AI can build the budget in chat, explain the choices, and adjust it with you.

2. Can I still create a budget myself?

Yes. Open Budgets, choose New, then set the budget name, dates, accounts, categories, and category limits yourself. This is useful if you already know exactly what you want and prefer to enter each limit manually.

3. Can Koody AI create a budget from my spending history?

Yes. If you already have transactions in Koody, Koody AI can use your spending history to build a budget that reflects how you actually spend. If you do not have enough data yet, it can ask you to import transactions or answer a few basic questions, so the first version is not just a guess.

4. What budget actions can I ask Koody AI to help with?

You can ask Koody AI to create a monthly budget, a weekly budget, a payday-aligned budget, a 50/30/20 budget, or a budget based on recent spending. You can also ask it to make a budget stricter or more relaxed, adjust category limits, change dates, edit a current budget, explain why a limit looks high or low, and help you keep refining the budget until it feels right.

5. Can I change accounts and categories after I create a budget?

While a budget is active, you can adjust accounts, categories, and limits, and Koody will recalculate based on the new setup. You can also ask Koody AI to help with those changes. After the budget expires, its structure is locked so the history stays consistent.

6. What happens when a budget expires?

When a budget reaches its end date, it expires and becomes read-only. You can still open it and view the original limits, transactions, charts, summaries, and notes, but you can no longer change the budget's structure.

7. Do I have to enter my income to create a budget in Koody?

No. Income is not required to create a budget. In Koody, a budget is a collection of categories with spending limits over a date range for specific accounts. You can decide your limits based on your income, your spending history, a goal, or whatever plan makes sense to you.

New here? Start tracking your spending in Koody today.